It’s virtually surreal that Amazon (NASDAQ: AMZN) shares misplaced 54% of their worth between mid-2021 and late 2022. Or maybe recency bias makes me assume it surreal as they’ve since bounced again in type, surging 180% to take the corporate’s market cap to a report $2.48trn.

Certainly, the inventory is up by a market-thrashing 25.4% in simply the previous three months! Which means an investor who was courageous sufficient to plonk down £20,000 in late October would now be sitting on round £25,080. That’s a improbable return in slightly below 14 weeks.

However are Amazon shares nonetheless price contemplating at present after this robust displaying? Let’s have a look.

Diversified enterprise

One of many issues I like about Amazon from an investing standpoint is its optionality. In different phrases, it has alternative ways to win past on-line retail. It operates the world’s main cloud computing platform, Amazon Net Providers (AWS), and generates income by promoting warehouse capability and logistics companies.

It additionally has a fast-growing digital promoting enterprise on its e-commerce app. Sellers pays to have their gadgets seem on the prime of search outcomes or on product pages. Amazon expenses them a charge every time somebody clicks on their sponsored itemizing. This can be a very worthwhile income stream, whereas the Prime subscription service retains clients coming again.

The corporate can also be investing in supply robots and drones, self-driving autos, numerous synthetic intelligence (AI) initiatives, and extra. Whereas these can weigh on near-term profitability, in addition they have the ability to spice up effectivity and margins over the long term.

Regardless of being 30 years previous and subsequently no spring rooster, Amazon remains to be one of the crucial thrilling corporations round, for my part.

Surging income

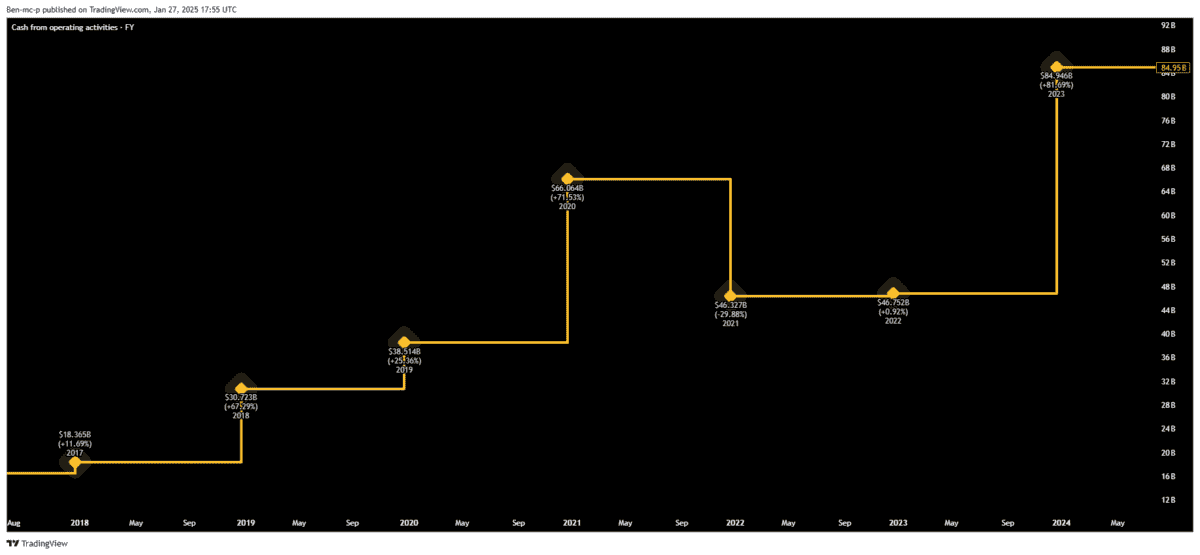

Lately, the corporate has turned itself right into a leaner beast. Consequently, its working cash flow is totally surging, as we will see beneath.

Plus, Wall Avenue analysts forecast double-digit income development over the following few years. In actual fact, the corporate stays on monitor to generate a mind-boggling $1trn in annual income by 2030! This assumes Amazon grows its prime line by roughly 8% yearly, which I feel is greater than life like.

That stated, nearing such a symbolic determine may deliver unfavourable headlines and extra regulatory scrutiny in future. Final yr, the US Federal Commerce Fee superior an antitrust lawsuit accusing Amazon of working an illegal monopoly. So potential regulation presents future dangers right here, I’d argue.

Is there any worth left?

Unsurprisingly, the inventory isn’t low-cost after its monster run. It’s buying and selling at 4 occasions gross sales, whereas the ahead price-to-earnings (P/E) ratio is 37.

But I feel that is cheap worth, contemplating the corporate’s revenue margins are anticipated to proceed increasing. The P/E ratio for 2026 drops to 31, primarily based on consensus forecasts.

Nonetheless, as we noticed in 2022, Amazon inventory may go down in addition to up. It has misplaced 50%+ of its worth on a number of events over the previous three many years. Subsequently, it’s best-suited to long-term buyers with a abdomen for volatility.

Trying forward over the following few years, I can solely see Amazon getting bigger as areas like e-commerce, digital promoting, and cloud computing increase worldwide.

Regardless of being at a report excessive, I feel the inventory is effectively price contemplating.

{kind=link}